Book Review: Standard Deviations, Flawed Assumptions, Tortured Data and Other Ways to Lie with Statistics

Years ago, when asked to recommend some good investment books, I often suggested ones dealing with the psychological issues influencing investor behavior. These focused on investor fear and greed, showing “what fools these mortals be.” Here are examples: Devil Take the Hindmost: A History of Financial Speculation by Edward Chancellor, and Extraordinary Popular Delusions and the Madness of […]

Why Does Dual Momentum Outperform?

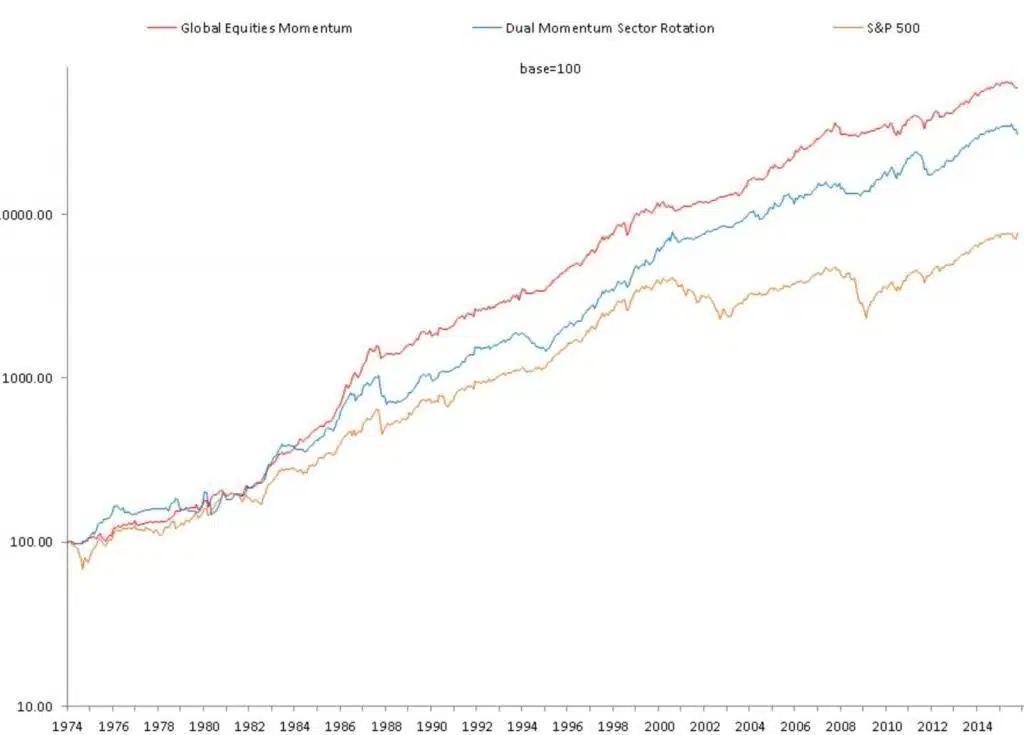

Those who have read my momentum research papers, book, and this blog should know that simple dual momentum has handily outperformed buy-and-hold. The following chart shows the 10-year rolling excess return of our popular Global Equities Momentum (GEM) dual momentum model compared to a 70/30 S&P 500/U.S. bond benchmark [1]. Results are hypothetical, are NOT […]

Bring More Data

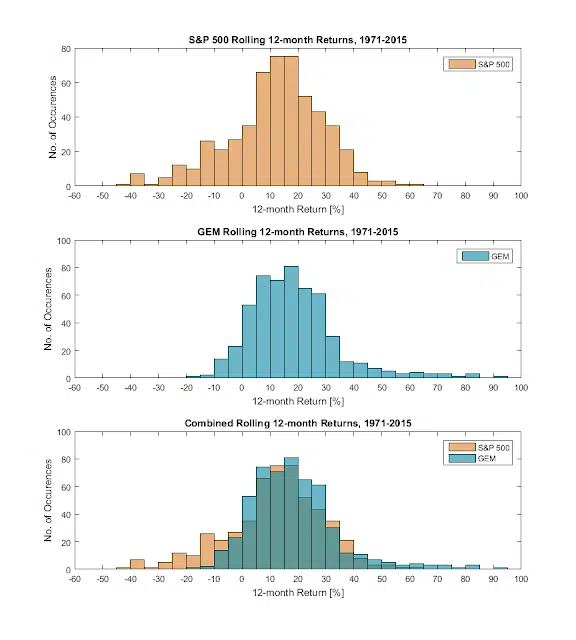

Several months ago we posted an article called “Bring Data” where we showed the importance of having abundant data for system development and validation. This was further reinforced to us recently when someone brought us additional U.S. stock sector data. Previously, we only had Morningstar sector data that went back to 1992, which we used to construct […]

Dual Momentum for non-US Investors

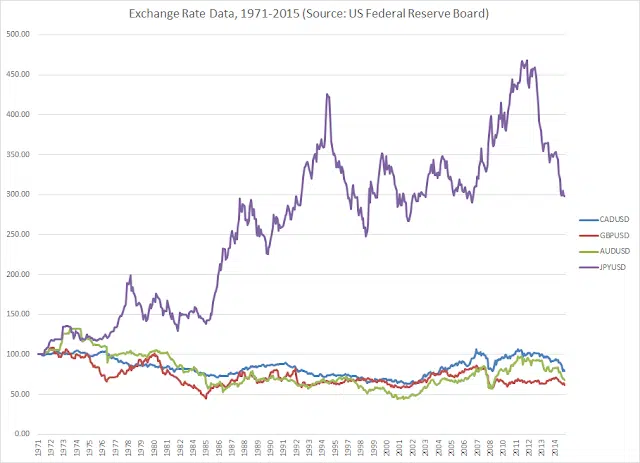

Gogi Grewal CFA is an analyst who has been following my work for years. He has an excellent grasp of dual momentum. Since Gogi lives in Canada, he researched the best ways for non-US investors to use momentum. Gogi has generously offered to share his findings with us here. I would add that if there […]

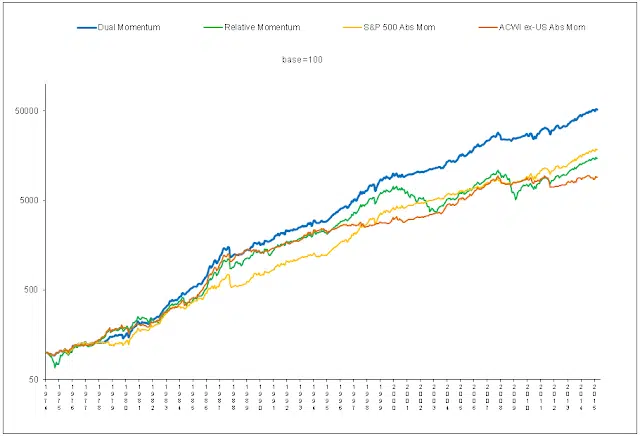

Dual, Relative & Absolute Momentum

Years ago when I first started studying momentum, two things stood out to me. The first was that most momentum research focused on cross-sectional stock studies. These looked at the future performance of stocks that had been strong versus stocks that had been weak. This was what interested academics most, since abnormal profit from strong […]